Managing the Employee Incentive Pool

Strategies every founder/CEO should consider when managing employee stock plans

Most employees join an early stage start up in the hopes that their individual stock options (ISOs) will be worth many millions someday. If they get in close enough to the ground floor their options may be pennies on the dollar (or less) relative to the exit value of the stock and may even have QSBS tax advantages too depending on when they exercise (I discuss at length here what that means).

Many first time founders and even serial entrepreneurs fail to really manage these pools well and will a) oversize the Employee Stock Option Pool (ESOP) by not negotiating, causing further dilution at each priced round; b) run out from not creating a plan and actively managing them along the way; c) not pay attention to 409a valuations or retaining QSBS rights that can help make the options more attractive. They lose track of the fact that these pools are not infinite and are a prime source of dilution over several rounds if not managed carefully. Not paying attention to the ESOP can make you less investible as anything you do valuation wise and limit your ability to attract key talent. The ESOP pool usually cannot be refreshed once it’s depleted without triggering painful anti-dilution provisions, so it’s important that the CEO and the CFO (if you are lucky enough to have one) really pay attention here.

Here’s an outline of how I’ve come to think about managing this process.

A quick refresher: options vs stock grants

Virtually all start up employees other than the founders receive their stock in the form of individual stock options (ISOs) which allow them to purchase their stock at some later day at a price that is locked in today (known as the Fair Market Value or the strike price) and significantly discounted to what investors are paying for them. These have favored tax treatment because you don’t have to pay taxes on the stock until you actually exercise them. These vary from Restricted Stock Units (RSUs) where stock is directly granted to the employee and they are taxed on it immediately as ordinary income.

Equity distribution must be an integral part of your hiring plan

While it’s fair to say that “no plan lasts past first contact with the enemy” it is important to have a hiring plan going into any raise. Even if you don’t have a detailed financial plan because it’s too early, you should be able to lay out approximately how many employees you’ll need to add to payroll, along with their positions and seniority.

A typical hiring plan including equity should look something like this:

First off some assumptions here about Acme.com. It has 2 founders and 13 existing employees. The company was started on January 1st 2020 (they had either really bad timing (covid) or really good timing (near top of the valuation bubble) depending on your perspective).

Tools exist out there such as PAVE and Option Impact (acquired by Pave in 2022), that can be purchased for a small fee (a few thousand dollars a year) or that you can access through one of your VCs that can help you gather the information to build this plan. They will give you statistics for any job position based on what stage your company is at and may even provide a tool to help you manage and build your equity plan (its a “fun” late night activity if you find building spreadsheets therapeutic).

A couple things to point out philosophically while we have the hood open here and are looking at the hiring plan in detail:

a) Salaries are a spectrum and always end up more than you think they will

I’ve used a continuum for future salaries here. This is because I’ve seldom been able to pay LESS than I thought I would for someone who I thought was a must hire. From the standpoint of budgeting you are best to use a more aggressive metric, like the 75th percentile of wages in the PAVE outputs so that you are raising enough money and aren’t planning to overhire.

b) Competent employees will try to place a monetary value on the options so you are best to anchor before they do

As a sanity check, you should look at the cash value of the options you are awarding to early employees using the 409a valuation as a good measure for how they will mentally value the options and weigh them against other job offers which will likely come with a cash bonus or retention bonus (the job they have already will probably pay one for them to stay). I realize this is also what they will pay to exercise those options, so essentially you are assuming that the common stock, as the average of a continuum of outcomes, will be valued as twice as much when they exercise as it is today.

Everyone knows working for a start up is risky - unless your company is literally “shit-hot”, it’s likely that people will discount the price versus what investors paid in the last round one or another as they try to figure out what it’s worth. So if you are trying to figure out the value at which people will value their options, the 409a strike price is as good a measure as any (and its defendable). This is also good for sanity checking the numbers that come out of PAVE or the database tools, which tend to have a high degree of variability. If you don’t think someone would find $10,000 worth of options as compelling, they probably won’t either and you need to give them a more generous option grant.

c) Show restraint handing out titles and don’t become too top heavy

You will almost certainly face the temptation to load up with very senior employees who are expensive too soon. This can make you very top heavy. If you find yourself wanting to hire more than one manager or director level person for every 10 employees, it’s probably too much and you’ll want to recalibrate. I also recommending holding off on hiring external managers rather than trying to hire them first since you should give your currently employees a chance to rise from within.

d) Think about refresh grants as part of your plan

As employees vest the number of shares or options they leave on the table diminishes. This gives them less incentive to stick around if a newer, hotter offer from a recruiter comes their way. Refresh grants are a great way to prevent that by ensuring that they continue to vest at a steady rate even as their original grants mature.

The refresh grant pool (including the founders) in the above example is larger than the new hire pool. If you remove the founders refresh however, this becomes smaller again by 3.75%. Unfortunately, most term sheets nowadays are more likely to recalculate/reset the founders vesting schedule than grant more shares (they know you have so much tied up in this, they don’t need to be more generous to get you to stay), but it’s not uncommon that founders coming near the end of their vesting period can negotiate some vesting for themselves if things are going well and it’s an up-round.

Now let’s double click on the refresh grants vis a vis employees:

Accounting for refresh grants in your plan

Assuming 18 months between priced raises (which is increasingly aggressive nowadays) you’ll need to make sure you keep enough in the pool to satisfy both your hiring plan as well as distribute refresh grants. What’s important to note in Table 1 is that refresh grants for employees (if you include a full refresh for the founders) is actually GREATER than the equity you plan on granting to new hires, assuming that the founders are expecting one too.

The first step is understanding what is market for these types of grants and it comes in a couple different philosophical flavors. There is one school of thought that says you should dole out option bonuses annually alongside cash bonuses and that you should typically reserve something like 25-50 basis points each year for share bonuses and then distribute them.

Another school of thought says that you should try to “maintain the same slope” of vesting so that employees have no incentive to leave after their first vesting period finishes. The problem with this approach is that its mathematically complex and may require long cliffs (18 mo or more if grants are occurring within 3 years of original share grants) that may bring scrutiny about the proper strike price applied.

The school of thought which I personally prefer and is the simplest for me to apply, is what I’ve heard many private equity firms use: a typical refresh grant is about 25% of the original grant at the conclusion of year three, along the same vesting schedule as before (i.e. one year cliff, 4 year vest is typically market). This is market in many sectors and ensures that while options are certainly front loaded, that there is significant vesting continuing long into your tenure if you choose to stay longer than four years.

Generally which school of thought you work with has a lot to do with who sits on your board/who your investors are. This is an area where you should probably have a board discussion as you are building your hiring plan, since these are the same people that will have to sign off on those grants later.

You can run a little hot - don’t assume everyone will work there for four years or fully vest

Now that I’ve scared you into making your plan super conservative by taking into account the actual present value of the stock, adding in refresh grants and resisting the urge to overtitle key hires, I’d like to give you a bit of a pressure relief valve. A key fact illustrated in this great chart below from Carta’s big data arm is that most start up employees will not still be around long enough to vest on even half of their options, much less refresh grants. As the chart below shows, 64% of employees have less than a 2 year tenure. For this reason you can afford to run a little hot and be generous, because as much as you hate to admit it today, you will have a fair number of your employees leave through attrition of one form or another.

Putting this all together: negotiating for a lower EIP percentage

I’ve been through nine different fundraises myself (from pre-seed to Series B) and advised others on at least a dozen more from pre-seed to Series C. With a fresh term sheet most people fixate on the obvious stuff: valuation, liquidation preference, committed cash, etc. But one other parameter that I’ve found is very important is the required allocation for the EIP. This is the stock pool you have to award to employees in addition to their cash compensation.

Since the same $1M is going to be a lot more expensive dilution-wise than it was before due to significantly lower valuations nowadays, founders should be looking for ways to minimize the dilution hit they take with each successive fundraising round. In a priced round such as a Seed, A or B typically a refresh of the Employee Incentive Pool (EIP) or Employee Stock Option Pool (ESOP) up to a certain percentage of the total diluted shares will be included.

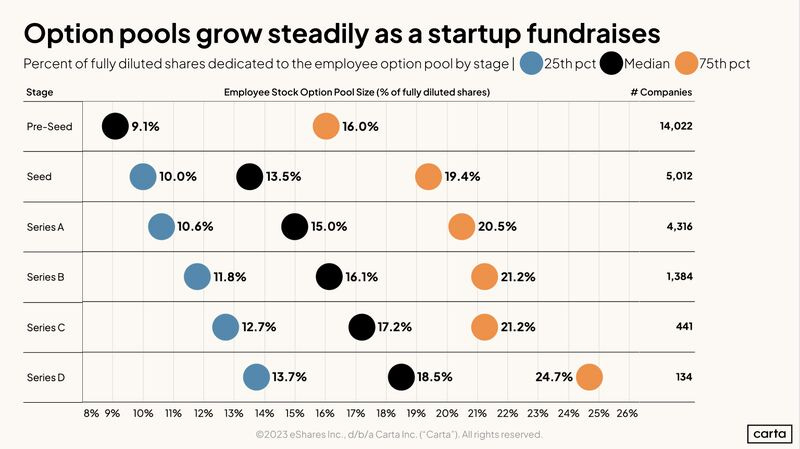

Depending on the stage of the round, this allocation may be anywhere from 20% (pre-seed or seed), 15% (A or B) or 10% or less. The pool size is pure dilution and impacts your share price that investors are paying in the round. A few obvious tactics in negotiation that you can use here:

First off, whatever is leftover in the pool from your last round should come off this number. So if you had 4% left in the pool, automatically take out 4%. That way 15% turns into a little less than 11% (because the 4% is off of your existing fully diluted share count, not the new one, the math gets a little better).

But you can get more aggressive that this as well if you use your hiring plan and its conclusions to justify a leaner pool. So using the example in the table above, you can actually make the case for 9%, especially if you are willing to forgo some of the founder refresh grants. This means that your original ownership becomes 6% higher and your share price goes up, which all the existing investors should approve of.

Data from Carta actually supports this as shown in Table 3. Even the 75th percentile of firms isn’t experiencing a 10% growth in the pool with each priced round, so it’s fair to negotiate this down to help defend your price per share -which the employees and investors will both thank you for).

Manage your advisors and review your advisory board every quarter

Successful start ups tend to collect advisors at the behest of investors looking to incentivize people in their network to put in a little time and help, founders and senior executives looking for “free” help (since options don’t burn cash on paper) or even investors that are looking for a way to sweeten the deal by tying an advisory contract to their (usually small) investment. In my experience, most advisors are somewhat helpful at first, but over time you get distracted and stop tasking them effectively or they get distracted and stop adding value. Meanwhile, market vesting for advisors is 3 years with no cliff, so they are usually vesting from day one and are continuing to eat away at your options pool whether you utilize them or not (it’s really an amazing gig if you can get it, don’t you think?).

For this reason, I recommend reviewing all your advisors at least twice a year to make sure they are still adding value (more often than this and you probably are playing a little too much “what have you done for me lately” for folks that you don’t call often. Sometimes advisors are so strategic that they are really just a Bat-phone you can pick up when you find yourself in a jam so judging them on a month by month basis if not realistic.

If advisors aren’t proving their worth, it’s time for a polite conversation that results in the termination of their contract. If they are smart and want their options (which they’ll now have to exercise or lose in 90 days) to be worth something, they’ll still help out occasionally. Otherwise, they probably weren’t helping you that much anyways. So long and thanks for all the fish!

Distinguishing warrants from NSOs

One other quick footnote: advisors get non-employee stock options (NSOs). Organizations that get stock options, get something called warrants instead. For instance, if you hire a lobbying firm and they ask for stock in lieu of payment, they are almost certainly getting warrants. They are some key differences (particularly with respect to board approval and dilution) that you need to understand that I’ll leave to you to study on on that with this great piece from Carta.

Conclusion

The employee stock pool is an incredibly valuable tool for hiring and needs to be balanced against the dilution it creates at every milestone where you touch the cap table. Active management of this pool can mean the difference of millions of dollars or more at exit and it’s essential that you put some forethought into how it integrates into your hiring plan. Don’t just build your hiring option plan in a vacuum - utilize industry tools and pressure test different strategies like refresh grant approaches with your board. You can opportunistically look for opportunities to cull options from zombie advisors or take into account that employee turnover is a fact of life to recover some of the ESOP over time. The reward for a solid track record of ESOP management is being able to ask for a smaller pool at each round, reducing dilution and giving you a better share price at each round.

Special thanks to Mike Palank, General Partner at Mac.vc for the edits and suggestions on this post, along with all my other start-up related posts. Maybe he’ll ask ChatGPT to rap this one too :-).